Gradient Boosted Regression Trees

Gradient Boosted Regression Trees (GBRT) or shorter Gradient Boosting is a flexible non-parametric statistical learning technique for classification and regression.

This notebook shows how to use GBRT in scikit-learn, an easy-to-use, general-purpose toolbox for machine learning in Python. We will start by giving a brief introduction to scikit-learn and its GBRT interface. The bulk of the tutorial will show how to use GBRT in practice and discuss important issues such as regularization, tuning, and model interpretation.

Gradient Boosted Regression Trees (GBRT) or shorter Gradient Boosting is a flexible non-parametric statistical learning technique for classification and regression.

This notebook shows how to use GBRT in scikit-learn, an easy-to-use, general-purpose toolbox for machine learning in Python. We will start by giving a brief introduction to scikit-learn and its GBRT interface. The bulk of the tutorial will show how to use GBRT in practice and discuss important issues such as regularization, tuning, and model interpretation.

Scikit-learn

Scikit-learn is a library that provides a variety of both supervised and unsupervised machine learning techniques as well as utilities for common tasks such as model selection, feature extraction, and feature selection.

Scikit-learn provides an object-oriented interface centered around the concept of an Estimator. According to the scikit-learn tutorial “An estimator is any object that learns from data; it may be a classification, regression or clustering algorithm or a transformer that extracts/filters useful features from raw data.” The API of an estimator looks roughly as follows:

In [1]:

class Estimator(object):

def fit(self, X, y=None):

"""Fits estimator to data. """

# set state of ``self``

return self

def predict(self, X):

"""Predict response of ``X``. """

# compute predictions ``pred``

return predThe Estimator.fit method sets the state of the estimator based on the training data. Usually, the data is comprised of a two-dimensional numpy array X of shape (n_samples, n_predictors) that holds the so-called feature matrix and a one-dimensional numpy array y that holds the responses (either class labels or regression values).

Estimators that can generate predictions provide an Estimator.predict method. In the case of regression, Estimator.predict will return the predicted regression values; it will return the corresponding class labels in the case of classification. Classifiers that can predict the probability of class membership have a method Estimator.predict_proba that returns a two-dimensional numpy array of shape (n_samples, n_classes) where the classes are lexicographically ordered.

In [2]:

from sklearn.ensemble import GradientBoostingClassifier, GradientBoostingRegressorEstimators support arguments to control the fitting behavior — these arguments are often called hyperparameters. Among the most important ones for GBRT are:

- number of regression trees (

n_estimators) - depth of each individual tree (

max_depth) - loss function (

loss) - learning rate (

learning_rate)

For example, if you want to fit a regression model with 100 trees of depth 3 using least-squares:

est = GradientBoostingRegressor(n_estimators=100, max_depth=3, loss='ls')You can find extensive documentation on the scikit-learn website or in the docstring of the estimator – in IPython simply use GradientBoostingRegressor? to view the docstring.

During the fitting process, the state of the estimator is stored in instance attributes that have a trailing underscore (‘_’). For example, the sequence of regression trees (sklearn.tree.DecisionTreeRegressor objects) is stored in est.estimators_.

Here is a self-contained example that shows how to fit a GradientBoostingClassifier to a synthetic dataset (taken from [Hastie et al., The Elements of Statistical Learning, Ed2]):

from sklearn.datasets import make_hastie_10_2

from sklearn.cross_validation import train_test_split

# generate synthetic data from ESLII - Example 10.2

X, y = make_hastie_10_2(n_samples=5000)

X_train, X_test, y_train, y_test = train_test_split(X, y)

# fit estimator

est = GradientBoostingClassifier(n_estimators=200, max_depth=3)

est.fit(X_train, y_train)

# predict class labels

pred = est.predict(X_test)

# score on test data (accuracy)

acc = est.score(X_test, y_test)

print('ACC: %.4f' % acc)

# predict class probabilities

est.predict_proba(X_test)[0]

ACC: 0.9240Out[4]:

<code>array([ 0.26442503, 0.73557497])</code>

Gradient Boosting in Practice

Most of the challenges in applying GBRT successfully in practice can be illustrated in the context of a simple curve fitting example. Below you can see a regression problem with one feature x and the corresponding response y. We draw 100 training data points by picking an x coordinate uniformly at random, evaluating the ground truth (sinoid function; light blue line) and then adding some random gaussian noise. In addition to the 100 training points (blue) we also draw 100 test data points (red) which we will use the evaluate our approximation.

In [5]:

import numpy as np

def ground_truth(x):

"""Ground truth -- function to approximate"""

return x * np.sin(x) + np.sin(2 * x)

def gen_data(n_samples=200):

"""generate training and testing data"""

np.random.seed(13)

x = np.random.uniform(0, 10, size=n_samples)

x.sort()

y = ground_truth(x) + 0.75 * np.random.normal(size=n_samples)

train_mask = np.random.randint(0, 2, size=n_samples).astype(np.bool)

x_train, y_train = x[train_mask, np.newaxis], y[train_mask]

x_test, y_test = x[~train_mask, np.newaxis], y[~train_mask]

return x_train, x_test, y_train, y_test

X_train, X_test, y_train, y_test = gen_data(200)

# plot ground truth

x_plot = np.linspace(0, 10, 500)

def plot_data(figsize=(8, 5)):

fig = plt.figure(figsize=figsize)

gt = plt.plot(x_plot, ground_truth(x_plot), alpha=0.4, label='ground truth')

# plot training and testing data

plt.scatter(X_train, y_train, s=10, alpha=0.4)

plt.scatter(X_test, y_test, s=10, alpha=0.4, color='red')

plt.xlim((0, 10))

plt.ylabel('y')

plt.xlabel('x')

plot_data(figsize=(8, 5))

If you fit an individual regression tree to the above data you get a piece-wise constant approximation. The deeper you grow the tree, the more constant segments you can accommodate and thus, the more variance you can capture.

In [6]:

from sklearn.tree import DecisionTreeRegressor

plot_data()

est = DecisionTreeRegressor(max_depth=1).fit(X_train, y_train)

plt.plot(x_plot, est.predict(x_plot[:, np.newaxis]),

label='RT max_depth=1', color='g', alpha=0.9, linewidth=2)est = DecisionTreeRegressor(max_depth=3).fit(X_train, y_train)

plt.plot(x_plot, est.predict(x_plot[:, np.newaxis]),

label='RT max_depth=3', color='g', alpha=0.7, linewidth=1)

plt.legend(loc='upper left')Out[6]:

Now, let’s fit a gradient boosting model to the training data and let’s see how the approximation progresses as we add more and more trees. The scikit-learn gradient boosting estimators allow you to evaluate the prediction of a model as a function of the number of trees via the staged_(predict|predict_proba) methods. These return a generator that iterates over the predictions as you add more and more trees.

In [7]:

from itertools import islice

plot_data()

est = GradientBoostingRegressor(n_estimators=1000, max_depth=1, learning_rate=1.0)

est.fit(X_train, y_train)

ax = plt.gca()

first = True

# step over prediction as we added 20 more trees.

for pred in islice(est.staged_predict(x_plot[:, np.newaxis]), 0, 1000, 10):

plt.plot(x_plot, pred, color='r', alpha=0.2)

if first:

ax.annotate('High bias - low variance', xy=(x_plot[x_plot.shape[0] // 2],

pred[x_plot.shape[0] // 2]),

xycoords='data',

xytext=(3, 4), textcoords='data',

arrowprops=dict(arrowstyle="->",

connectionstyle="arc"))

first = False

pred = est.predict(x_plot[:, np.newaxis])

plt.plot(x_plot, pred, color='r', label='GBRT max_depth=1')

ax.annotate('Low bias - high variance', xy=(x_plot[x_plot.shape[0] // 2],

pred[x_plot.shape[0] // 2]),

xycoords='data', xytext=(6.25, -6),

textcoords='data', arrowprops=dict(arrowstyle="->",

connectionstyle="arc"))

plt.legend(loc='upper left')Out[7]:

The above plot shows 50 red lines where each shows the response of the GBRT model after 20 trees have been added. It starts with a very crude approximation that can only fit more-or-less constant functions (i.e. High bias – low variance) but as we add more trees the more variance our model can capture resulting in the solid red line.

We can see that the more trees we add to our GBRT model and the deeper the individual trees are the more variance we can capture thus the higher the complexity of our model. But as usual in machine learning model complexity comes at a price — overfitting.

An important diagnostic when using GBRT in practice is the so-called deviance plot that shows the training/testing error (or deviance) as a function of the number of trees.

In [8]:

>

n_estimators = len(est.estimators_)

def deviance_plot(est, X_test, y_test, ax=None, label='', train_color='#2c7bb6',

test_color='#d7191c', alpha=1.0):

"""Deviance plot for ``est``, use ``X_test`` and ``y_test`` for test error. """

test_dev = np.empty(n_estimators)

for i, pred in enumerate(est.staged_predict(X_test)):

test_dev[i] = est.loss_(y_test, pred)

if ax is None:

fig = plt.figure(figsize=(8, 5))

ax = plt.gca()

ax.plot(np.arange(n_estimators) + 1, test_dev, color=test_color, label='Test %s' % label,

linewidth=2, alpha=alpha)

ax.plot(np.arange(n_estimators) + 1, est.train_score_, color=train_color,

label='Train %s' % label, linewidth=2, alpha=alpha)

ax.set_ylabel('Error')

ax.set_xlabel('n_estimators')

ax.set_ylim((0, 2))

return test_dev, ax

test_dev, ax = deviance_plot(est, X_test, y_test)

ax.legend(loc='upper right')

# add some annotations

ax.annotate('Lowest test error', xy=(test_dev.argmin() + 1, test_dev.min() + 0.02), xycoords='data',

xytext=(150, 1.0), textcoords='data',

arrowprops=dict(arrowstyle="->", connectionstyle="arc"),

)

ann = ax.annotate('', xy=(800, test_dev[799]), xycoords='data',

xytext=(800, est.train_score_[799]), textcoords='data',

arrowprops=dict(arrowstyle=""))

ax.text(810, 0.25, 'train-test gap')Out[8]:

The blue line above shows the training error: it rapidly decreases in the beginning and then gradually slows down but keeps decreasing as we add more and more trees. The testing error (red line) too decreases rapidly in the beginning but then slows down and reaches its minimum fairly early (~50 trees) and then even starts increasing. This is what we call overfitting, at a certain point the model has so much capacity that it starts fitting the idiosyncrasies of the training data — in our case the random gaussian noise component that we added — and hence limiting its ability to generalize to new unseen data. A large gap between training and testing error is usually a sign of overfitting.

The great thing about gradient boosting is that it provides a number of knobs to control overfitting. These are usually subsumed by the term regularization.

Regularization

GBRT provide three knobs to control overfitting: tree structure, shrinkage, and randomization.

Tree Structure

The depth of the individual trees is one aspect of model complexity. The depth of the trees basically control the degree of feature interactions that your model can fit. For example, if you want to capture the interaction between a feature latitude and a feature longitude your trees need a depth of at least two to capture this. Unfortunately, the degree of feature interactions is not known in advance but it is usually fine to assume that it is fairly low — in practice, a depth of 4-6 usually gives the best results. In scikit-learn you can constrain the depth of the trees using the max_depth argument.

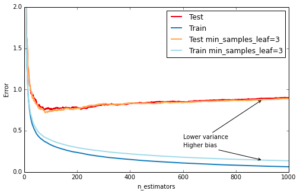

Another way to control the depth of the trees is by enforcing a lower bound on the number of samples in a leaf: this will avoid unbalanced splits where a leaf is formed for just one extreme data point. In scikit-learn you can do this using the argument min_samples_leaf. This is effectively a means to introduce bias into your model with the hope to also reduce variance as shown in the example below:

In [9]:

def fmt_params(params):

return ", ".join("{0}={1}".format(key, val) for key, val in params.iteritems())

fig = plt.figure(figsize=(8, 5))

ax = plt.gca()

for params, (test_color, train_color) in [({}, ('#d7191c', '#2c7bb6')),

({'min_samples_leaf': 3},

('#fdae61', '#abd9e9'))]:

est = GradientBoostingRegressor(n_estimators=n_estimators, max_depth=1, learning_rate=1.0)

est.set_params(**params)

est.fit(X_train, y_train)

test_dev, ax = deviance_plot(est, X_test, y_test, ax=ax, label=fmt_params(params),

train_color=train_color, test_color=test_color)

ax.annotate('Higher bias', xy=(900, est.train_score_[899]), xycoords='data',

xytext=(600, 0.3), textcoords='data',

arrowprops=dict(arrowstyle="->", connectionstyle="arc"),

)

ax.annotate('Lower variance', xy=(900, test_dev[899]), xycoords='data',

xytext=(600, 0.4), textcoords='data',

arrowprops=dict(arrowstyle="->", connectionstyle="arc"),

)

plt.legend(loc='upper right')Out[9]:

Shrinkage

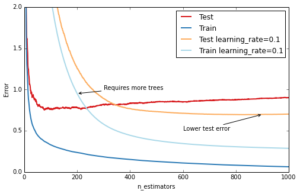

The most important regularization technique for GBRT is shrinkage: the idea is basically to do slow learning by shrinking the predictions of each individual tree by some small scalar, the learning_rate. By doing so the model has to re-enforce concepts. A lower learning_rate requires a higher number of n_estimators to get to the same level of training error — so its trading runtime against accuracy.

In [10]:

fig = plt.figure(figsize=(8, 5))

ax = plt.gca()

for params, (test_color, train_color) in [({}, ('#d7191c', '#2c7bb6')),

({'learning_rate': 0.1},

('#fdae61', '#abd9e9'))]:

est = GradientBoostingRegressor(n_estimators=n_estimators, max_depth=1, learning_rate=1.0)

est.set_params(**params)

est.fit(X_train, y_train)

test_dev, ax = deviance_plot(est, X_test, y_test, ax=ax, label=fmt_params(params),

train_color=train_color, test_color=test_color)

ax.annotate('Requires more trees', xy=(200, est.train_score_[199]), xycoords='data',

xytext=(300, 1.0), textcoords='data',

arrowprops=dict(arrowstyle="->", connectionstyle="arc"),

)

ax.annotate('Lower test error', xy=(900, test_dev[899]), xycoords='data',

xytext=(600, 0.5), textcoords='data',

arrowprops=dict(arrowstyle="->", connectionstyle="arc"),

)

plt.legend(loc='upper right')Out[10]:

Stochastic Gradient Boosting

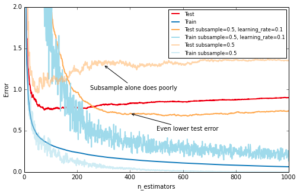

Similar to RandomForest, introducing randomization into the tree building process can lead to higher accuracy. Scikit-learn provides two ways to introduce randomization: a) subsampling the training set before growing each tree (subsample) and b) subsampling the features before finding the best split node (max_features). Experience showed that the latter works better if there is a sufficient large number of features (>30). One thing worth noting is that both options reduce runtime.

Below we show the effect of using subsample=0.5, i.e. growing each tree on 50% of the training data, on our toy example:

In [11]:

fig = plt.figure(figsize=(8, 5)) ax = plt.gca() for params, (test_color, train_color) in [({}, ('#d7191c', '#2c7bb6')),

({'learning_rate': 0.1, 'subsample': 0.5},

('#fdae61', '#abd9e9'))]:

est = GradientBoostingRegressor(n_estimators=n_estimators, max_depth=1, learning_rate=1.0,

random_state=1)

est.set_params(**params)

est.fit(X_train, y_train)

test_dev, ax = deviance_plot(est, X_test, y_test, ax=ax, label=fmt_params(params),

train_color=train_color, test_color=test_color)

ax.annotate('Even lower test error', xy=(400, test_dev[399]), xycoords='data',

xytext=(500, 0.5), textcoords='data',

arrowprops=dict(arrowstyle="->", connectionstyle="arc"),

)

est = GradientBoostingRegressor(n_estimators=n_estimators, max_depth=1, learning_rate=1.0,

subsample=0.5)

est.fit(X_train, y_train)

test_dev, ax = deviance_plot(est, X_test, y_test, ax=ax, label=fmt_params({'subsample': 0.5}),

train_color='#abd9e9', test_color='#fdae61', alpha=0.5)

ax.annotate('Subsample alone does poorly', xy=(300, test_dev[299]), xycoords='data',

xytext=(250, 1.0), textcoords='data',

arrowprops=dict(arrowstyle="->", connectionstyle="arc"),

)

plt.legend(loc='upper right', fontsize='small')Out[11]:

Hyperparameter tuning

We now have introduced a number of hyperparameters — as usual in machine learning it is quite tedious to optimize them. Especially, since they interact with each other (learning_rate and n_estimators, learning_rate and subsample, max_depth and max_features).

We usually follow this recipe to tune the hyperparameters for a gradient boosting model:

- Choose

lossbased on your problem at hand (ie. target metric) - Pick

n_estimatorsas large as (computationally) possible (e.g. 3000). - Tune

max_depth,learning_rate,min_samples_leaf, andmax_featuresvia grid search. - Increase

n_estimatorseven more and tunelearning_rateagain holding the other parameters fixed.

Scikit-learn provides a convenient API for hyperparameter tuning and grid search:

In [12]:

from sklearn.grid_search import GridSearchCV

param_grid = {'learning_rate': [0.1, 0.05, 0.02, 0.01],

'max_depth': [4, 6],

'min_samples_leaf': [3, 5, 9, 17],

# 'max_features': [1.0, 0.3, 0.1] ## not possible in our example (only 1 fx)

}

est = GradientBoostingRegressor(n_estimators=3000)

# this may take some minutes

gs_cv = GridSearchCV(est, param_grid, n_jobs=4).fit(X_train, y_train)

# best hyperparameter setting

gs_cv.best_params_Out[12]:

<code>{‘learning_rate’: 0.05, ‘max_depth’: 6, ‘min_samples_leaf’: 5}</code>

Use-case: California Housing

This use-case study shows how to apply GBRT to a real-world dataset. The task is to predict the log median house value for census block groups in California. The dataset is based on the 1990 census comprising roughly 20.000 groups. There are 8 features for each group including: median income, average house age, latitude, and longitude. To be consistent with [Hastie et al., The Elements of Statistical Learning, Ed2] we use Mean Absolute Error as our target metric and evaluate the results on an 80-20 train-test split.

In [13]:

import pandas as pd

from sklearn.datasets.california_housing import fetch_california_housing

cal_housing = fetch_california_housing()

# split 80/20 train-test

X_train, X_test, y_train, y_test = train_test_split(cal_housing.data,

np.log(cal_housing.target),

test_size=0.2,

random_state=1)

names = cal_housing.feature_namesSome of the aspects that make this data set challenging are: a) heterogeneous features (different scales and distributions) and b) non-linear feature interactions (specifically latitude and longitude). Furthermore, the data contains some extreme values of the response (log median house value) — such a data set strongly benefits from robust regression techniques such as huberized loss functions.

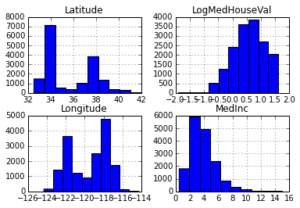

Below you can see histograms for some of the features and the response. You can see that they are quite different: median income is left skewed, latitude and longitude are bi-modal, and log median house value is right skewed.

In [14]:

import pandas as pd

X_df = pd.DataFrame(data=X_train, columns=names)

X_df['LogMedHouseVal'] = y_train

_ = X_df.hist(column=['Latitude', 'Longitude', 'MedInc', 'LogMedHouseVal'])

Lets fit a GBRT model to this dataset and inspect the model

In [15]:

est = GradientBoostingRegressor(n_estimators=3000, max_depth=6, learning_rate=0.04,

loss='huber', random_state=0)

est.fit(X_train, y_train)Out[15]:

GradientBoostingRegressor(alpha=0.9, init=None, learning_rate=0.04,

loss='huber', max_depth=6, max_features=None,

max_leaf_nodes=None, min_samples_leaf=1, min_samples_split=2,

n_estimators=3000, random_state=0, subsample=1.0, verbose=0,

warm_start=False)In [16]:

from sklearn.metrics import mean_absolute_error mae = mean_absolute_error(y_test, est.predict(X_test))

print('MAE: %.4f' % mae)Feature importance

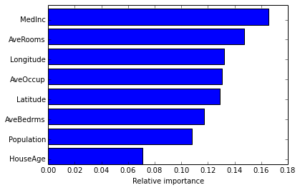

Often features do not contribute equally to predict the target response. When interpreting a model, the first question usually is: what are those important features and how do they contributing in predicting the target response?

A GBRT model derives this information from the fitted regression trees which intrinsically perform feature selection by choosing appropriate split points. You can access this information via the instance attribute est.feature_importances_.

In [17]:

# sort importances

indices = np.argsort(est.feature_importances_)

# plot as bar chart

plt.barh(np.arange(len(names)), est.feature_importances_[indices])

plt.yticks(np.arange(len(names)) + 0.25, np.array(names)[indices])

_ = plt.xlabel('Relative importance')

Partial dependence

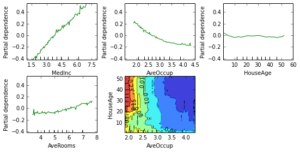

Partial dependence plots show the dependence between the response and a set of features, marginalizing over the values of all other features. Intuitively, we can interpret the partial dependence as the expected response as a function of the features we conditioned on.

The plot below contains 4 one-way partial dependence plots (PDP) each showing the effect of an individual feature on the response. We can see that median income MedInc has a linear relationship with the log median house value. The contour plot shows a two-way PDP. Here we can see an interesting feature interaction. It seems that house age itself has hardly any effect on the response but when AveOccup is small it has an effect (the older the house the higher the price).

In [18]:

from sklearn.ensemble.partial_dependence import plot_partial_dependence features = ['MedInc', 'AveOccup', 'HouseAge', 'AveRooms',

('AveOccup', 'HouseAge')]

fig, axs = plot_partial_dependence(est, X_train, features,

feature_names=names, figsize=(8, 6))

Scikit-learn provides a convenience function to create such plots: sklearn.ensemble.partial_dependence.plot_partial_dependence or a low-level function that you can use to create custom partial dependence plots (e.g. map overlays or 3d plots). More detailed information can be found here.

Get Started Today.